Resources

About Us

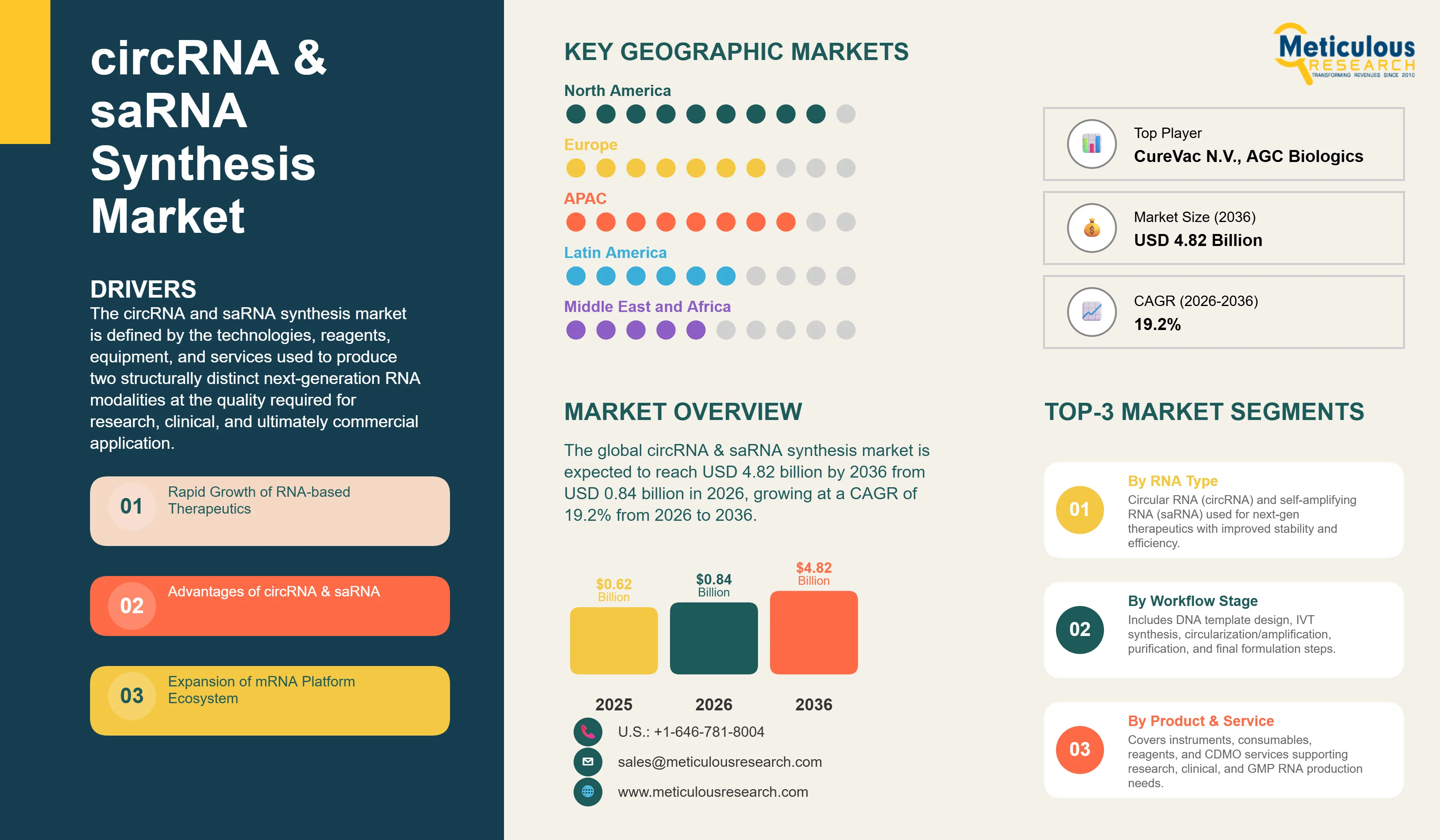

The global circRNA & saRNA synthesis market was valued at USD 0.62 billion in 2025. This market is expected to reach USD 4.82 billion by 2036 from USD 0.84 billion in 2026, growing at a CAGR of 19.2% from 2026 to 2036.

The growth of this market is driven by the emergence of two next-generation RNA modalities, circular RNA and self-amplifying RNA, that address fundamental limitations of conventional linear mRNA therapeutics in durability of protein expression, dose efficiency, and manufacturing economics. Circular RNA is a covalently closed RNA molecule with no free 5' or 3' ends, which confers exceptional resistance to exonucleolytic degradation and extends intracellular half-life substantially beyond that of linear mRNA. Self-amplifying RNA is an engineered RNA molecule derived from alphavirus genomes that incorporates the viral RNA-dependent RNA polymerase machinery, enabling the molecule to self-replicate within the transfected cell and sustain high-level antigen or protein expression from a fraction of the dose required for conventional mRNA. Both modalities are attracting significant scientific and commercial interest as platforms for vaccines, gene therapy, protein replacement, and cancer immunotherapy, and the synthesis, purification, and formulation technologies required to produce them at clinical and commercial quality define the circRNA and saRNA synthesis market.

The broader RNA therapeutics landscape provides the commercial context for this emerging market. According to a peer-reviewed review published in PubMed Central (Cell Reports Medicine, May 2024), as of 2024 there were 17 FDA-approved RNA therapeutics and more than 222 ongoing clinical trials of RNA-based medicines across antisense oligonucleotides, siRNA, mRNA, and emerging modalities. The first FDA-approved RNA therapeutics dates to 1998 with fomivirsen, and the class has grown substantially over the subsequent decades, culminating in the approval of mRNA COVID-19 vaccines from Pfizer-BioNTech and Moderna under the Emergency Use Authorization in 2020 and full approval as Comirnaty and Spikevax in 2022. This established regulatory and clinical infrastructure for RNA therapeutics provides the commercial and scientific foundation on which circRNA and saRNA synthesis technologies are being built and commercialized.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The circRNA and saRNA synthesis market is defined by the technologies, reagents, equipment, and services used to produce two structurally distinct next-generation RNA modalities at the quality required for research, clinical, and ultimately commercial application. Circular RNA is produced through a synthesis workflow that begins with the design and production of a DNA template encoding the desired RNA sequence with splice sites or ribozyme sequences flanking the region to be circularized. The template is transcribed by in vitro transcription to produce a linear RNA precursor, which is then circularized through one of several chemical or enzymatic approaches including splint-mediated ligation using T4 RNA ligase, group I or group II intron-based self-splicing, chemical phosphoramidite ligation, or the use of the permuted group I ribozyme system developed by researchers at the Wesselhoeft laboratory and widely adopted in the field. The circularized product is then purified by HPLC or denaturing gel electrophoresis to remove residual linear precursors, characterized by analytical methods including gel electrophoresis, mass spectrometry, and RNase R treatment, and formulated in lipid nanoparticles or other delivery vehicles for in vivo application.

Self-amplifying RNA is produced by in vitro transcription of a DNA template encoding both the alphavirus non-structural protein replicase complex, most commonly derived from Venezuelan Equine Encephalitis Virus or Sindbis virus, and the therapeutic antigen or protein of interest. The resulting saRNA molecule is substantially larger than conventional mRNA, typically 9,000 to 12,000 nucleotides compared with 1,000 to 4,000 for linear mRNA vaccines, which presents unique challenges for IVT yield, purification, and quality control. Because saRNA molecules self-amplify within transfected cells through the action of the encoded replicase, the effective dose required to achieve a given level of protein expression is substantially lower than for conventional mRNA, enabling dose reduction of 10-fold to 100-fold compared with equivalent linear mRNA constructs. The ARCT-154 saRNA COVID-19 vaccine, which received the world's first regulatory approval for a saRNA vaccine from Japan's Pharmaceuticals and Medical Devices Agency on November 27, 2023, and began real-world distribution in Japan in October 2024, contains 100 micrograms of saRNA per dose, a dose that demonstrates the self-amplifying mechanism enabling meaningful immunological response from a relatively low RNA mass.

The competitive landscape of the circRNA and saRNA synthesis market spans RNA therapeutics developers who own the proprietary platforms, reagent and enzyme suppliers that provide the IVT systems and circularization kits, CDMO organizations that provide synthesis services, and analytical and formulation technology companies. Arcturus Therapeutics is the most clinically advanced saRNA developer, with ARCT-154 already approved and distributed in Japan. Moderna and BioNTech, leveraging their established mRNA manufacturing infrastructure, are active in next-generation RNA formats including saRNA. CureVac has saRNA programs in its pipeline. In the circRNA space, Orna Therapeutics, Laronde, and Circular Genomics are among the companies advancing circRNA expression platforms toward clinical programs. On the synthesis technology and services side, TriLink BioTechnologies, Aldevron, Maravai LifeSciences, and WuXi AppTec provide IVT reagents, custom RNA synthesis, and GMP manufacturing services that support the circRNA and saRNA development ecosystem.

World's First saRNA Vaccine Approval Validates the Platform for Broader Clinical Development

The approval of ARCT-154 as the world's first saRNA vaccine by Japan's Pharmaceuticals and Medical Devices Agency on November 27, 2023, represents the most significant commercial and regulatory milestone in the history of self-amplifying RNA technology and directly validates saRNA as a viable therapeutic platform for broad clinical and commercial development. According to a peer-reviewed analysis published in PubMed Central (2025), ARCT-154 demonstrated effectiveness in terms of magnitude, persistence, and breadth of immune response that was superior to the conventional mRNA vaccine BNT162b2 in its pivotal Phase 3 clinical trial, with similar or less frequent adverse events. Real-world distribution of ARCT-154 under the brand name KOSTAIVE, manufactured by Meiji Seika Pharma in Japan, began in October 2024, according to the same NIH-indexed peer-reviewed source. The approval further received authorization by the European Medicines Agency in 2025, marking the first saRNA vaccine approval in Europe and confirming that the regulatory pathway for saRNA products is viable across multiple major regulatory jurisdictions. These approvals establish the manufacturing, analytical, and regulatory precedents that subsequent saRNA vaccine and therapeutic programs can build upon, reducing the technical and regulatory risk for new entrants and accelerating investment in saRNA synthesis technology and CDMO capacity.

circRNA Attracting Increasing Research and Commercial Investment as a Superior Protein Expression Platform

Circular RNA is attracting growing scientific and commercial investment as a protein expression platform that addresses the fundamental durability limitation of linear mRNA, where the absence of a 5' cap and poly-A tail protection in circRNA provides inherent resistance to exonucleolytic degradation that extends intracellular protein expression duration substantially beyond linear mRNA. According to a peer-reviewed review published in PubMed Central indexed by NIH (Advances in RNA-based therapeutics, Frontiers in Molecular Biosciences, 2025), early-phase clinical trials are actively exploring circular RNA as an expression platform with enhanced stability and translational efficiency. Orna Therapeutics, which has developed proprietary oRNA technology for protein expression from circular RNA, advanced its first circRNA program into clinical development in 2024. Laronde, which raised substantial venture capital funding for its Endless RNA technology platform based on circular RNA, is pursuing multiple programs in oncology and rare diseases. The combination of superior stability, potential for reduced dosing frequency compared with linear mRNA, and the ability to express complex proteins from a single circular RNA molecule is driving increasing research investment at academic institutions funded through NIH grants and at biotechnology companies seeking to differentiate from the established linear mRNA platform.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 4.82 Billion |

|

Market Size in 2026 |

USD 0.84 Billion |

|

Market Size in 2025 |

USD 0.62 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 19.2% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

RNA Type, Workflow Stage, Product and Service, Technology Platform, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Commercial Validation of RNA Therapeutics and Expanding Clinical Pipeline

The primary driver of the circRNA and saRNA synthesis market is the commercial validation of the broader RNA therapeutics platform and the expanding clinical pipeline that is creating growing demand for next-generation RNA synthesis technologies. According to a peer-reviewed review published in PubMed Central (Cell Reports Medicine, May 2024), as of 2024 there were 17 FDA-approved RNA therapeutics across multiple modalities and more than 222 RNA therapeutic clinical trials actively ongoing, with antisense oligonucleotide-based therapies alone having progressed through 100 Phase 1 trials with 25% advancing to Phase 2 and 3 development. The clinical success of mRNA COVID-19 vaccines from Pfizer-BioNTech and Moderna demonstrated to regulators, investors, and the pharmaceutical industry that RNA-based medicines can be manufactured at scale, delivered safely, and reviewed rapidly under established regulatory frameworks, creating the institutional confidence and infrastructure base upon which circRNA and saRNA programs are being built. According to an NIH-indexed peer-reviewed review published in PubMed Central (Journal of the American Chemical Society, 2023), RNA-based medicines are designed to target disease-causing genetic elements that are considered undruggable by conventional small molecules and antibodies, representing a fundamentally expanded therapeutic target space that motivates continued investment in the RNA platform broadly and in next-generation modalities including circRNA and saRNA specifically.

Opportunity: CDMO Infrastructure Expansion for Next-generation RNA Modalities

The expansion of CDMO capabilities to support circRNA and saRNA synthesis at clinical and GMP scale represents a significant opportunity for contract manufacturing organizations already established in the linear mRNA manufacturing space. The COVID-19 vaccine manufacturing programs executed by CDMOs including WuXi AppTec, AGC Biologics, TriLink BioTechnologies, and Aldevron demonstrated the industrial feasibility of large-scale RNA synthesis and lipid nanoparticle formulation and built the specialized workforce, equipment infrastructure, and regulatory compliance systems required for GMP RNA production. These capabilities provide a strong foundation for adapting manufacturing processes to circRNA and saRNA synthesis, which shares the IVT-based synthesis workflow of linear mRNA while requiring additional specialized steps for circularization and enhanced purification. The EMA Draft Guideline on Quality, Nonclinical and Clinical Requirements for Investigational Advanced Therapy Medicinal Products, released in its second version in 2024 as noted in an NIH-indexed symposium report (Toxicologic Pathology, December 2024), is developing the regulatory quality framework for saRNA as an advanced therapy medicinal product, providing increasing regulatory clarity for CDMOs seeking to establish GMP-compliant saRNA synthesis capabilities for the European market.

Why Does Self-amplifying RNA Lead the Market?

In 2026, the self-amplifying RNA (saRNA) segment is expected to account for the largest share of the circRNA & saRNA synthesis market. This is mainly because saRNA technology is currently more developed than circular RNA (circRNA). A significant milestone was reached in November 2023 when ARCT-154 became the first saRNA product to get regulatory approval from Japan’s Pharmaceuticals and Medical Devices Agency (PMDA). The product later gained authorization from the European Medicines Agency (EMA) in 2025. According to a 2025 peer-reviewed study published in PubMed Central, ARCT-154 showed a stronger immune response compared to conventional mRNA vaccines during Phase 3 trials and began commercial distribution in Japan in October 2024. Another important development came from Gennova Biopharmaceuticals. Their saRNA COVID-19 vaccine, GEMCOVAC-19, received restricted emergency use authorization in India in 2022. These approvals have boosted confidence in the saRNA platform and increased demand for saRNA synthesis capabilities. Additionally, saRNA production uses the same in-vitro transcription setup already built for linear mRNA production. This allows existing RNA manufacturers and CDMOs to expand into saRNA production without needing major new investments, aiding quicker commercial adoption.

However, the circular RNA (circRNA) segment is expected to grow the fastest during the forecast period. Interest in circRNA is rising due to its strong technical benefits, especially its higher stability compared to linear RNA technologies. This makes circRNA very suitable for applications that need long-lasting protein expression, including protein replacement therapies, gene therapies, and cancer vaccines. Companies such as Orna Therapeutics are moving forward with early-stage clinical programs and collecting important validation data for the platform. According to a 2025 NIH-indexed review published in Frontiers, early clinical trials are actively studying circular RNA because of its better stability and translation efficiency. As circRNA technologies progress in clinical development, demand for GMP-grade circRNA synthesis services and specialized production technologies is expected to grow rapidly in the coming years.

How Does RNA Synthesis Lead the Workflow Market?

In 2026, the RNA synthesis stage is expected to hold the largest share of the circRNA and saRNA synthesis market. In vitro transcription is the main production step for both circular RNA and self-amplifying RNA. It uses T7 or SP6 RNA polymerase to create the encoded RNA sequence from a linearized DNA template. This step consumes the largest amounts of enzyme, nucleotides, and buffer reagents in the synthesis workflow. It also needs the most advanced temperature-controlled reactor systems and process monitoring equipment. The IVT step also highlights saRNA's unique manufacturing challenges: the large size of saRNA molecules, typically 9,000 to 12,000 nucleotides, reduces IVT yield per reaction volume compared to shorter linear mRNA products. This makes yield optimization in the IVT step the main focus of manufacturing process development for saRNA. TriLink BioTechnologies, Aldevron, and Maravai LifeSciences are the main commercial suppliers of GMP-grade T7 RNA polymerase and modified nucleotide mixtures for clinical-grade IVT. This makes the RNA synthesis stage the largest revenue-generating workflow step for reagent suppliers in the market.

However, the purification and quality control stage is expected to show the fastest growth during the forecast period. Purifying circRNA and saRNA presents more complex challenges than purifying linear mRNA, and increased investment to tackle these challenges is driving technology and service revenue in this workflow segment. CircRNA purification must separate the covalently closed circular product from linear RNA precursors, splicing by-products, and other impurities. This is done using methods like HPLC, RNase R digestion of residual linear RNA, and high-resolution electrophoresis. Regulatory focus on RNA product characterization, including showing circularization efficiency, the absence of linear precursors, and measuring double-stranded RNA contaminants, is driving investment in analytical quality control methods and tools for circRNA products. For saRNA, the dsRNA contaminants created as replication intermediates during the self-amplification process represent an immunostimulatory impurity that needs to be removed or minimized through purification. Developing scalable HPLC methods for dsRNA removal from large saRNA molecules is an active area of investment in process development.

Why Do Services Lead the Market?

In 2026, the services segment is expected to hold the largest share of the circRNA & saRNA synthesis market. Contract synthesis and process development services provided by CDMOs represent the primary commercial pathway for circRNA and saRNA development programs to access GMP-quality RNA for clinical trials. The specialized technical knowledge required to optimize circularization efficiency, remove linear RNA precursors at scale, produce saRNA at clinical grade with controlled dsRNA content, and formulate RNA in lipid nanoparticles is concentrated in a small number of specialist CDMOs and synthesis service providers including TriLink BioTechnologies, Aldevron, WuXi AppTec, and AGC Biologics. For most circRNA and saRNA developers, accessing this expertise through CDMO service agreements is substantially more efficient than building equivalent in-house synthesis capability, which requires significant capital investment in RNA synthesis equipment, clean-room infrastructure, and a workforce with scarce expertise in advanced RNA manufacturing processes.

However, the consumables and reagents segment is expected to witness the fastest growth during the forecast period. As the number of circRNA and saRNA programs in research and clinical development grows, the recurring demand for T7 RNA polymerase, nucleotide triphosphates, GTP analogs such as the anti-reverse cap analog used in saRNA synthesis, circularization enzymes including T4 RNA ligase 2, ribozyme components, LNP lipid components, and analytical kits expands proportionally with program volume. Maravai LifeSciences through its TriLink BioTechnologies subsidiary, Aldevron, and Merck KGaA are positioned as the primary beneficiaries of this consumable demand growth, as they supply the critical reagent components used in both research-scale and GMP-scale RNA synthesis workflows globally.

How Do IVT-based Synthesis Platforms Lead the Market?

In 2026, the IVT-based synthesis platforms segment is expected to hold the largest share of the circRNA & saRNA synthesis market. In vitro transcription is the universal first step in the production of both circular RNA and self-amplifying RNA, and the IVT platform infrastructure developed for linear mRNA manufacturing during the COVID-19 vaccine production scale-up represents an established technology base that can be applied to next-generation RNA synthesis with process modifications. CDMOs that invested heavily in IVT platform scale-up and GMP validation during 2020 to 2023 for mRNA vaccine manufacturing are able to redirect this capacity toward circRNA and saRNA synthesis, providing the market with a larger installed base of IVT manufacturing capability than would exist if these RNA types were developing in isolation. The dominance of IVT-based synthesis is also reflected in the commercial product portfolios of reagent suppliers, where IVT enzyme systems, nucleotide mixtures, and template DNA preparation kits represent the largest revenue categories.

However, the LNP and delivery technologies segment is expected to witness the fastest growth during the forecast period. Lipid nanoparticle formulation technology is the rate-limiting delivery step for both circRNA and saRNA, and the optimization of LNP composition, particle size, and surface characteristics for the specific physicochemical properties of circular RNA and large saRNA molecules is an active area of technology development with significant commercial value. The larger size of saRNA molecules and the distinct topology of circRNA compared with linear mRNA require LNP formulation parameters that are not directly transferable from established mRNA LNP processes, driving investment in new LNP composition screening and optimization. The FDA's regulatory guidance on LNP-formulated RNA products, which has been developed through the review of mRNA COVID-19 vaccine applications, provides a regulatory reference framework for saRNA LNP product characterization that developers and CDMOs are applying to circRNA and saRNA LNP formulation development programs.

Why Does the Vaccines Application Lead the Market?

In 2026, the vaccines segment is expected to hold the largest share of the circRNA & saRNA synthesis market. Vaccine development is the most commercially advanced application for saRNA technology, anchored by the regulatory approval and commercial distribution of ARCT-154 in Japan and its subsequent authorization by the EMA. According to a peer-reviewed review published in PubMed Central (Self-Amplifying RNA: A Second Revolution of mRNA Vaccines against COVID-19, PMC, 2024), ARCT-154 received authorization from Japan's Pharmaceuticals and Medical Devices Agency on November 27, 2023, and demonstrated immune responses superior to the conventional mRNA vaccine BNT162b2 against Omicron variants in its Phase 3 clinical trial. The same source confirmed that GEMCOVAC-19, a human COVID-19 saRNA vaccine developed by Gennova Biopharmaceuticals, received authorization for restricted emergency use in India in 2022, establishing two regulatory precedents for saRNA vaccines across different jurisdictions. The plug-and-play adaptability of the saRNA platform, where only the antigen-encoding sequence needs to be changed while the replicase machinery remains constant, makes it particularly well suited to rapid vaccine development for emerging infectious disease threats and for personalized cancer vaccine programs targeting patient-specific neoantigen profiles.

However, the gene therapy segment is expected to witness the fastest growth during the forecast period. Both circRNA and saRNA offer distinct advantages over viral vector gene therapy platforms for applications requiring sustained transgene expression. CircRNA provides durable protein expression without genomic integration risk, viral immunogenicity, or the manufacturing complexity of viral vector production. saRNA enables high-level, self-amplifying transgene expression from low initial doses, potentially addressing the cost and dose limitations that constrain the accessibility of viral vector gene therapies. According to an NIH-indexed peer-reviewed review (Advances in RNA-based therapeutics, Frontiers, 2025), early-phase clinical trials are exploring circular RNA for gene therapy applications, and the convergence of RNA gene therapy programs with established LNP delivery technology is expected to drive growing demand for circRNA and saRNA synthesis in the gene therapy application during the forecast period.

Why Do Biopharmaceutical Companies Lead the End User Market?

In 2026, the biopharmaceutical companies segment is expected to hold the largest share of the circRNA & saRNA synthesis market. Innovator biopharmaceutical companies are the primary funders of circRNA and saRNA therapeutic programs and the primary procurers of synthesis services, reagents, and equipment for clinical-stage RNA production. Arcturus Therapeutics, the developer of the approved ARCT-154 saRNA vaccine and multiple additional saRNA therapeutic candidates in its pipeline, is the most commercially advanced saRNA biopharmaceutical company. Moderna, which holds extensive mRNA manufacturing and delivery technology intellectual property and has disclosed saRNA programs as part of its next-generation RNA platform development, represents the largest-revenue RNA biopharmaceutical company and a significant potential driver of saRNA synthesis demand. BioNTech SE is pursuing circRNA and saRNA platforms as part of its broader RNA therapeutics portfolio following its mRNA vaccine commercial success. CureVac N.V. has saRNA programs in infectious disease and oncology applications.

However, the CDMOs and CMOs segment is expected to witness the fastest growth during the forecast period. CDMOs are rapidly expanding their capabilities to serve the circRNA and saRNA synthesis market, representing the highest-growth end-user segment for synthesis technology and reagent suppliers. WuXi AppTec has developed RNA synthesis capabilities including circular RNA services. AGC Biologics is expanding its RNA manufacturing offerings. The growth of the CDMO market for circRNA and saRNA synthesis is supported by the EMA's 2024 Draft Guideline on quality requirements for investigational advanced therapy medicinal products, which is creating regulatory clarity for CDMOs establishing GMP-compliant circRNA and saRNA synthesis processes for the European clinical trial market. As more circRNA and saRNA programs advance toward clinical development, the CDMO sector will capture an increasing share of synthesis service revenue.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global circRNA & saRNA synthesis market. The United States is the primary market, driven by the concentration of RNA therapeutics companies including Arcturus Therapeutics, Moderna, BioNTech US operations, CureVac US programs, Orna Therapeutics, and Laronde, the largest base of NIH-funded academic research programs in RNA biology and RNA therapeutics, and the most developed mRNA manufacturing and CDMO infrastructure that is being adapted to circRNA and saRNA synthesis.

According to a peer-reviewed review published in PubMed Central (Cell Reports Medicine, May 2024), more than 222 clinical trials of RNA therapeutics were ongoing as of 2024, with the United States hosting the majority of early-phase RNA therapeutic trials registered on ClinicalTrials.gov. NIH-funded research programs at leading U.S. academic institutions including MIT, Stanford, Harvard, and the University of Pennsylvania have generated foundational circRNA biology discoveries and saRNA engineering advances that form the scientific basis for current commercial circRNA and saRNA platforms. The FDA's established regulatory framework for RNA therapeutics, including the review of linear mRNA COVID-19 vaccines under both EUA and full BLA pathways, has created the regulatory precedents that saRNA and circRNA developers in the United States can build upon for their clinical development and regulatory strategies.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the circRNA & saRNA synthesis market during the forecast period. This growth is driven by Japan's position as the jurisdiction that issued the world's first saRNA vaccine regulatory approval, China's expanding RNA therapeutics research and CDMO sector, and government-supported RNA manufacturing capacity investment across the region.

Japan holds a unique position in the global saRNA market as the jurisdiction of the world's first regulatory approval of a saRNA vaccine. According to peer-reviewed sources indexed by NIH and PubMed, ARCT-154 received full approval from Japan's Pharmaceuticals and Medical Devices Agency on November 27, 2023, and real-world distribution under the brand name KOSTAIVE manufactured by Meiji Seika Pharma began in October 2024. This approval establishes Japan as a first-mover regulatory market for saRNA products and is likely to attract saRNA clinical development programs seeking to leverage Japan's established saRNA regulatory precedent. The approval also confirms that Japan's PMDA has developed the scientific assessment capability to evaluate saRNA vaccine applications, providing a regulatory pathway reference for other saRNA developers globally. China's growing RNA therapeutics sector, supported by domestic companies including GenScript Biotech and the WuXi group's RNA synthesis capabilities, is expanding circRNA and saRNA research activity and CDMO service capacity. India's Gennova Biopharmaceuticals, whose GEMCOVAC-19 saRNA COVID-19 vaccine received emergency authorization in India in 2022, represents the only other approved saRNA vaccine product globally alongside ARCT-154, establishing India as a second regulatory precedent jurisdiction for saRNA in the Asia-Pacific region.

Some of the key companies operating in the global circRNA & saRNA synthesis market are Moderna, Inc., BioNTech SE, CureVac N.V., Arcturus Therapeutics Holdings Inc., Gritstone bio, Inc., eTheRNA Immunotherapies NV, Ethris GmbH, Orbital Therapeutics, Laronde Inc., TriLink BioTechnologies, Aldevron (Danaher), AGC Biologics, WuXi AppTec, GenScript Biotech Corporation, and Maravai LifeSciences.

The global circRNA & saRNA synthesis market is expected to grow from USD 0.84 billion in 2026 to USD 4.82 billion by 2036.

The global circRNA & saRNA synthesis market is projected to grow at a CAGR of 19.2% from 2026 to 2036.

The self-amplifying RNA segment is expected to dominate the overall market in 2026, supported by the world's first saRNA vaccine approval by Japan's PMDA in November 2023 and the EMA authorization of ARCT-154 in 2025. However, the circular RNA segment is expected to witness the fastest CAGR, driven by growing investment in circRNA as a superior stability protein expression platform and the entry of circRNA programs from Orna Therapeutics and Laronde into clinical development.

The vaccines segment is expected to dominate the overall market in 2026, anchored by the regulatory approval and commercial distribution of ARCT-154 in Japan, EMA authorization in 2025, and the emergency authorization of GEMCOVAC-19 in India. However, the gene therapy segment is expected to witness the fastest CAGR, driven by the advantages of circRNA and saRNA over viral vectors for sustained transgene expression without genomic integration risk.

North America is expected to lead the global market in 2026. However, Asia-Pacific is expected to witness the fastest CAGR, driven by Japan's position as the world's first saRNA vaccine approval jurisdiction, China's expanding RNA CDMO sector, and India's GEMCOVAC-19 emergency authorization establishing a second Asia-Pacific regulatory precedent for saRNA.

The major players are Moderna, BioNTech SE, CureVac, Arcturus Therapeutics, Gritstone bio, eTheRNA Immunotherapies, Ethris, Orbital Therapeutics, Laronde, TriLink BioTechnologies, Aldevron (Danaher), AGC Biologics, WuXi AppTec, GenScript Biotech, and Maravai LifeSciences.

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Market Ecosystem

1.4 Currency and Limitations

1.4.1 Currency

1.4.2 Limitations

1.5 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Forecast Modeling

2.4 Data Triangulation

2.5 Assumptions

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rapid Growth of RNA-based Therapeutics

4.2.1.2 Advantages of circRNA & saRNA

4.2.1.3 Expansion of mRNA Platform Ecosystem

4.2.1.4 Increasing Vaccine Development Activities

4.2.2 Restraints

4.2.2.1 Early-stage Market with Limited Commercialization

4.2.2.2 Manufacturing Complexity

4.2.2.3 Regulatory Uncertainty

4.2.3 Opportunities

4.2.3.1 Next-generation Vaccines (saRNA-based)

4.2.3.2 Gene Therapy Applications

4.2.3.3 AI-driven RNA Design Platforms

4.2.3.4 Expansion of CDMO Capabilities

4.2.4 Challenges

4.2.4.1 Scale-up and Purification Challenges

4.2.4.2 Delivery System Limitations

4.3 Technology & Synthesis Landscape

4.3.1 In Vitro Transcription (IVT)

4.3.2 Circularization Techniques (Enzymatic & Chemical)

4.3.3 Self-amplifying RNA Engineering

4.3.4 RNA Modification & Stabilization Techniques

4.3.5 Lipid Nanoparticle (LNP) Delivery Systems

4.3.6 Automation & Digital RNA Design

4.4 circRNA & saRNA Ecosystem

4.4.1 RNA Therapeutics Companies

4.4.2 CDMOs/CMOs

4.4.3 Reagent & Technology Providers

4.4.4 Academic & Research Institutes

4.4.5 Pharmaceutical Companies

4.5 Value Chain Analysis

4.5.1 Template Design (DNA Constructs)

4.5.2 RNA Synthesis (IVT)

4.5.3 Circularization / Amplification

4.5.4 Purification & Quality Control

4.5.5 Formulation & Delivery

4.6 Regulatory Landscape

4.6.1 Regulatory Framework for RNA Therapeutics

4.6.2 Clinical Trial Guidelines

4.6.3 GMP Requirements for RNA Manufacturing

4.7 Industry Trends

4.7.1 Rise of Self-amplifying RNA Vaccines

4.7.2 Increasing Investment in circRNA Platforms

4.7.3 Expansion of RNA CDMO Infrastructure

4.7.4 Integration of AI in RNA Design

4.8 Cost and Pricing Analysis

4.8.1 Cost by RNA Type (circRNA vs saRNA)

4.8.2 Manufacturing Cost Breakdown

4.8.3 CDMO Pricing Models

5. circRNA & saRNA Synthesis Market, by RNA Type

5.1 Introduction

5.2 Circular RNA (circRNA)

5.3 Self-amplifying RNA (saRNA)

6. circRNA & saRNA Synthesis Market, by Workflow Stage

6.1 Introduction

6.2 Template Design & DNA Synthesis

6.3 RNA Synthesis (IVT)

6.4 Circularization / Amplification

6.5 Purification & Quality Control

6.6 Formulation & Delivery

7. circRNA & saRNA Synthesis Market, by Product & Service

7.1 Introduction

7.2 Instruments & Equipment

7.2.1 IVT Systems

7.2.2 Purification Systems

7.2.3 Analytical Instruments

7.3 Consumables & Reagents

7.3.1 Enzymes & Kits

7.3.2 Nucleotides & Buffers

7.3.3 LNP Formulation Reagents

7.4 Services

7.4.1 Contract Manufacturing (CDMO/CMO)

7.4.2 Process Development Services

7.4.3 Analytical & QC Services

8. circRNA & saRNA Synthesis Market, by Technology Platform

8.1 IVT-based Synthesis Platforms

8.2 Enzymatic Circularization Technologies

8.3 Chemical Circularization Technologies

8.4 Self-amplifying RNA Engineering Platforms

8.5 LNP & Delivery Technologies

9. circRNA & saRNA Synthesis Market, by Application

9.1 Introduction

9.2 Vaccines

9.2.1 Infectious Disease Vaccines

9.2.2 Cancer Vaccines

9.3 Gene Therapy

9.4 Protein Replacement Therapy

9.5 Immunotherapy

9.6 Research Applications

10. circRNA & saRNA Synthesis Market, by End User

10.1 Biopharmaceutical Companies

10.2 Biotechnology Companies

10.3 CDMOs/CMOs

10.4 Academic & Research Institutes

11. circRNA & saRNA Synthesis Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Sweden

11.3.8 Switzerland

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Rest of MEA

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Technology Innovators

12.4.3 Emerging Players

12.5 Market Ranking/Positioning Analysis

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Moderna, Inc.

13.2 BioNTech SE

13.3 CureVac N.V.

13.4 Arcturus Therapeutics Holdings Inc.

13.5 Gritstone bio, Inc.

13.6 eTheRNA Immunotherapies NV

13.7 Ethris GmbH

13.8 Orbital Therapeutics

13.9 Laronde Inc.

13.10 TriLink BioTechnologies

13.11 Aldevron (Danaher)

13.12 AGC Biologics

13.13 WuXi AppTec

13.14 GenScript Biotech Corporation

13.15 Maravai LifeSciences

14. Appendix

14.1 Customization Options

14.2 Related Reports

Published Date: Aug-2024

Published Date: Jan-2025

Subscribe to get the latest industry updates